Over-the-Counter (OTC) markets are decentralized marketplaces where securities, commodities, and derivatives are traded directly between buyers and sellers without going through a centralized exchange. These markets are often characterized by their lack of standardized trading platforms and regulations.

OTC market regulations aim to provide a framework for these transactions, ensuring market integrity, transparency, and investor protection. However, due to the decentralized nature of OTC markets, regulation can be challenging.

Key Aspects of OTC Market Regulations

- Trade Reporting: Many jurisdictions require participants in OTC markets to report trades to regulatory authorities. This helps to improve market transparency and facilitate surveillance. Accurate reporting relies on access to evidential OTC data.

- Clearing and Settlement: Central counterparties (CCPs) can be used to clear and settle OTC derivatives contracts, reducing counterparty risk.

- Capital Requirements: Regulatory authorities often impose capital requirements on financial institutions that engage in OTC activities, to ensure their financial stability.

- Conduct Standards: Rules may be in place to govern the conduct of market participants, such as preventing market manipulation and insider trading.

- Product Oversight: Certain OTC products, such as complex derivatives, may be subject to specific regulatory oversight to mitigate risks. Effective product oversight often depends on independent derivatives valuations, which support transparency, valuation governance, and regulatory expectations.

How OTC Market Regulations Work

The exact implementation of OTC market regulations varies across jurisdictions. However, a common approach involves:

- Issuance of Regulations: Regulatory authorities publish rules and guidelines governing OTC market activities.

- Registration and Supervision: Financial institutions that participate in OTC markets may be required to register with regulators and are subject to ongoing supervision.

- Enforcement: Regulators have the power to investigate and enforce compliance with OTC market regulations, which can include fines, sanctions, or even criminal charges.

Challenges in Regulating OTC Markets

- Decentralization: The decentralized nature of OTC markets makes it difficult to monitor and regulate all transactions.

- Complexity: OTC products can be highly complex, making it challenging to develop effective regulations.

- Global Nature: OTC markets often involve participants from multiple jurisdictions, making international cooperation essential.

Enforcement of Financial OTC Regulations

The enforcement of Financial OTC regulations is a complex task that involves various strategies and tools. Regulatory authorities employ a combination of proactive and reactive measures to ensure compliance and deter misconduct. To manage these regulatory expectations, firms increasingly rely on structured OTC compliance solutions that support oversight, reporting, and governance.

Key Enforcement Strategies

-

Surveillance and Monitoring:

- Trade Reporting: Regulatory authorities analyze trade data reported by market participants to identify potential irregularities or suspicious activity.

- Electronic Surveillance: Advanced technology is used to monitor market activity for signs of manipulation, fraud, or other misconduct. This often includes the use of trading analytics for regulatory monitoring to identify unusual patterns and potential misconduct.

- Risk Assessments: Regulators assess the risk profiles of financial institutions and market participants to identify potential vulnerabilities.

-

Inspections and Examinations:

- On-Site Inspections: Regulatory authorities conduct on-site inspections of financial institutions to assess their compliance with OTC regulations and identify potential deficiencies.

- Document Reviews: Regulators examine internal documents, records, and procedures to ensure compliance with regulatory requirements.

-

Investigations:

- Complaints and Tips: Regulators investigate complaints from investors, market participants, or other sources.

- Market Surveillance: Investigations may be initiated based on suspicious market activity or patterns.

- Cooperation with Law Enforcement: Regulators may collaborate with law enforcement agencies to investigate serious violations.

-

Enforcement Actions:

- Cease and Desist Orders: Regulators can issue cease and desist orders to require firms to stop engaging in illegal or harmful activities.

- Fines and Penalties: Financial institutions that violate OTC regulations may be subject to significant fines or penalties.

- Disciplinary Actions: Regulatory authorities can take disciplinary actions against individuals who engage in misconduct.

- Criminal Referrals: In cases of serious violations, regulators may refer matters to law enforcement agencies for criminal prosecution.

-

Regulatory Guidance and Education:

- Issuance of Guidance: Regulators publish guidance and interpretive letters to clarify regulatory requirements and expectations.

- Educational Programs: Regulatory authorities may conduct educational programs to help market participants understand their obligations and best practices.

Challenges in Enforcement

- Complexity of OTC Products: The complexity of many OTC products can make it difficult to detect and investigate violations.

- Global Nature of OTC Markets: The global nature of OTC markets can make it challenging to coordinate enforcement efforts across different jurisdictions.

- Technological Advancements: Rapid technological advancements can create new challenges for regulators in terms of monitoring and enforcement.

Despite these challenges, effective enforcement of Financial OTC regulations is crucial to maintaining market integrity and protecting investors. The penalties for non-compliance with Financial OTC regulations can vary depending on the jurisdiction, the severity of the violation, and the regulatory authority involved. However, they can be significant and may include:

-

Financial Penalties:

- Fines: Regulatory authorities can impose substantial fines on financial institutions that violate OTC regulations. The amount of the fine may be calculated based on the severity of the violation, the size of the institution, and other factors.

- Restitution: In some cases, regulators may require financial institutions to make restitution to investors who have suffered losses due to violations.

-

Disciplinary Actions:

- Cease and Desist Orders: Regulatory authorities can issue cease and desist orders requiring firms to stop engaging in illegal or harmful activities.

- Suspension or Revocation of Licenses: In serious cases, regulators may suspend or revoke the licenses of financial institutions or individuals who have violated OTC regulations.

- Prohibitions from Engaging in Certain Activities: Regulators may prohibit individuals from engaging in certain activities within the financial industry.

-

Criminal Penalties:

- Criminal Charges: In cases of serious violations, regulators may refer matters to law enforcement agencies for criminal prosecution. Individuals convicted of criminal offenses related to OTC market violations may face imprisonment, fines, or other penalties.

The penalties for non-compliance with Financial OTC regulations can vary depending on the jurisdiction, the severity of the violation, and the regulatory authority involved. However, they can be significant and may include:

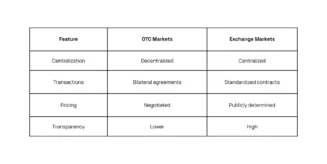

OTC vs. Exchange Markets

Over-the-Counter (OTC) markets and exchange markets are two primary venues for trading securities, commodities, and derivatives. While both serve as marketplaces, they operate in distinct ways.

OTC Markets

- Decentralized: OTC markets are decentralized, meaning there’s no central physical location or exchange. Trades are executed directly between buyers and sellers.

- Bilateral Agreements: Transactions in OTC markets are based on bilateral agreements between counterparties.

- Negotiated Prices: Prices are negotiated between the buyer and seller, often based on factors such as market conditions, creditworthiness, and the size of the transaction.

- Limited Transparency: OTC markets generally have less transparency than exchange markets, as trade information is not publicly disclosed in real-time.

- Higher Counterparty Risk: Due to the bilateral nature of OTC transactions, there’s a higher risk of one party failing to fulfill their obligations.

Exchange Markets

- Centralized: Exchange markets are centralized, with a physical or electronic platform where trades are executed.

- Standardized Contracts: Transactions are based on standardized contracts, ensuring uniformity and facilitating price discovery.

- Public Pricing: Prices are determined through a competitive bidding process and are publicly disseminated in real-time.

- Lower Counterparty Risk: Exchange markets typically have lower counterparty risk as transactions are cleared through a central clearinghouse.

- Regulatory Oversight: Exchange markets are subject to stricter regulatory oversight than OTC markets.

Key Differences Summarized

OTC markets are primarily used for trading a variety of non-exchange-listed securities . These can include:

- Corporate Bonds: Bonds issued by corporations, which are typically not listed on a stock exchange.

- Municipal Bonds: Bonds issued by state and local governments, often to fund infrastructure projects or public services.

- Derivatives: Financial instruments that derive their value from an underlying asset, such as futures, options, and swaps.

- Foreign Exchange: Currencies traded between countries.

- Repo Securities: Short-term loans backed by securities.

- Custom-Tailored Securities: Securities that are created to meet the specific needs of a particular investor or group of investors.

While some stocks may also be traded OTC, they are typically less liquid and have higher transaction costs compared to stocks traded on major exchanges.

FAQs about OTC Market Regulations

Are OTC markets regulated?

Yes, OTC markets are regulated, but generally less strictly than traditional exchanges. In the U.S., the Financial Industry Regulatory Authority (FINRA) oversees OTC broker‑dealers and trading activity, while overall transparency and investor protections tend to be lower than on centralized exchanges.

This lighter regulatory environment increases risks such as limited disclosures, higher volatility, and potential manipulation.

Additionally, OTC markets operate within a decentralized structure, making compliance and oversight more complex globally.

Who regulates OTC markets?

OTC markets are regulated by multiple authorities, depending on the type of instrument and jurisdiction:

United States:

- SEC oversees securities laws and compliance.

- FINRA regulates broker‑dealers and trading conduct.

- CFTC oversees OTC derivatives and swap markets.

Other jurisdictions:

Oversight is typically carried out by national financial regulators (e.g., ESMA in the EU, ASIC in Australia), often supported by trade reporting requirements and conduct‑of‑business rules.

Does the SEC regulate OTC markets?

Yes. The SEC regulates OTC securities, setting the federal framework for disclosure, fair trading, and fraud prevention. For example, Rule 15c2‑11 governs when broker‑dealers may publish quotations for OTC securities, requiring sufficient publicly available issuer information.

The SEC also enforces registration, exemptions, resale rules, and reporting obligations (e.g., Rule 144 for restricted securities).

What is the EMIR regulation for OTC derivatives?

The European Market Infrastructure Regulation (EMIR) is the EU’s primary framework governing OTC derivatives. It was introduced to reduce systemic risk after the 2008 financial crisis and applies to both financial and non‑financial counterparties. Key requirements include:

- Mandatory trade reporting of all derivatives to trade repositories.

- Central clearing of standardized OTC derivatives through CCPs.

- Risk‑mitigation requirements (e.g., margin exchange, timely confirmations) for non‑cleared trades.

- Operational risk controls and transparency obligations.

EMIR also includes mechanisms for recognizing non‑EU CCPs and trade repositories, ensuring EU‑equivalent standards internationally.

What information gets reported in OTC trades?

OTC trade reporting requirements depend on the jurisdiction, but globally they include details that improve transparency for regulators:

- Trade economics: price, quantity, execution time.

- Counterparty information and roles.

- Product identifiers (e.g., UTI, UPI).

- Collateral and margin details (in some regimes).

- Clearing status: cleared vs. non‑

For example, FINRA mandates timely reporting of OTC equity transactions to TRFs/ORFs, including time, price, share quantity, and capacity.

Derivatives regimes such as CFTC Part 43/45 and EMIR require comprehensive swap data reporting to trade repositories, covering lifecycle events, collateral, and position data.

How are OTC markets regulated across different countries?

OTC regulation looks different around the world. In the U.S., agencies like the SEC, CFTC, and FINRA impose detailed reporting and conduct rules, creating a relatively robust oversight environment.

In the EU, EMIR sets out strict requirements for reporting, clearing, and risk‑mitigation in OTC derivatives markets, alongside separate rules for OTC consumer products. Across Asia, regulatory frameworks tend to shift more frequently, requiring firms to monitor changes closely.

Studies comparing regions show wide differences in transparency and pre‑market requirements, with the EU generally taking a more stringent, authorization‑focused approach than the U.S. monograph‑style system. Overall, OTC regulation varies significantly depending on local policy priorities and market maturity.

Disclaimer

© 2026 ICAP Information Services Limited (“IISL”). This communication is provided by ICAP Information Services Limited or a member of its group (“Parameta”) and all information contained in or attached hereto (the “Information”) is for information purposes only and is confidential. Access to the Information by anyone other than the intended recipient is unauthorised without Parameta’s prior written approval. The Information may not be not used or disclosed for any purpose without Parameta’s prior written approval, including without limitation, storing, copying, distributing, licensing, selling or displaying the Information, using the Information in an application or to create derived data of any kind, co-mingling the Information with any other data or using the data for any unlawful purpose of for any purpose that would cause it to become a benchmark under any law, regulation or guidance. The Information is not, and should not be construed as, a live price, an offer, bid, recommendation or solicitation in relation to any financial instrument or investment or to participate in any particular trading strategy or constituting financial or investment advice or a financial promotion. The Information does not constitute a public offer under any applicable legislation or an offer to sell or a solicitation of an offer to buy any securities. The Information is not to be relied upon for any purpose whatsoever and is provided “as is” without warranty of any kind, either expressly or by implication, including without limitation as to completeness, timeliness, accuracy, continuity, merchantability or fitness for any particular purpose. All representations and warranties are expressly disclaimed, to the fullest extent possible under applicable law. In no circumstances will Parameta be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the Information. Parameta may suspend, withdraw or modify or change the terms of the provision of the Information at any time in its sole discretion, without notice. All rights, including without limitation intellectual property rights, in and to the Information are, and shall remain, the property of IISL or its licensors. Use of, access to or delivery of Parameta’s products and/or services requires a prior written licence from Parameta or its relevant affiliates. The terms of this disclaimer are governed by the laws of England and Wales.