Seventy‑three days into the Iran war, clarity remains in short supply. Initial expectations of containment have faded, replaced by a situation that oscillates between escalation and restraint, leaving markets and policymakers alike navigating an unresolved equilibrium.

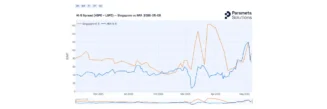

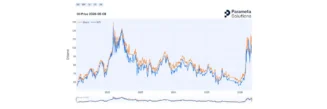

The initial price shocks can be seen in refined products such as diesel, jet fuel and bunker fuel, as well as in prompt prices for the two main crude benchmarks, Brent and West Texas Intermediate (WTI). Bunker fuel is trading at roughly double its pre-war level, which is broadly in line with expectations.

What is unexpected, however, is that bunker fuel currently trades at roughly the same level in Singapore as in ARA (Amsterdam-Rotterdam-Antwerp). The impact would be expected to fall more heavily on Asian markets. US Energy Information Administration (EIA) data put roughly 84% of crude moving through the Strait of Hormuz in 2024 as Asia-bound, and the initial spike in Singapore bunker prices, which briefly tripled, appeared to confirm that view.

Oil, however, is a global commodity, and Asian buyers did not wait long before redirecting their tankers to the Americas and bidding for WTI barrels, the key U.S. benchmark. That surge in demand pushed WTI higher, briefly trading above Brent.

Filled storage facilities in the Gulf, shut-in wells and tankers trapped or diverted to the Americas argue against a quick resumption of production and delivery, even in the evet of a peace agreement.

The disruption has also rippled through a range of other critical commodities, including sulfur, a by‑product of oil and gas processing, along with helium and natural gas. Estimates suggest that as much as 30% of global urea trade has been removed from supply chains due to disruption in the Strait of Hormuz, an impact exacerbated by sulfur shortages at the outset of the spring planting season.

Market participants are now starting to price in higher inflation. Inflation expectation swaps, a derivative brokered at TP ICAP, are moving higher and pointing to elevated inflation over the next one to two years.

The world’s central bankers and rates traders are equally starting to shift. The 29 April 2026 Federal Open Market Committee (FOMC) meeting featured a rare 8-4 vote to hold the target range at 3.50%-3.75%, the highest dissent count since 1992. Three of the four dissenters, regional Fed presidents Hammack, Kashkari and Logan, objected to language in the statement suggesting a bias toward future easing, arguing it was inappropriate given inflationary pressures, while the fourth, Governor Miran, dissented in favor of a 25 bp cut.

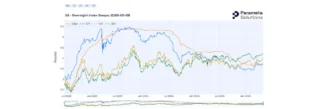

The market remained calm after the decision, as a hold was widely expected and priced in. Overnight Index Swaps on SOFR (Secured Overnight Financing Rate), anchored by the Fed funds rate, stayed steady at the front-end.

The US overnight index swaps term structure is now fully inverted. The long end at 30Y looks poised to break out, while the front-end 3M tenor appears to have found a floor near 3.6% and the 1Y tenor a floor near 3.8%.

One wild card to watch, the weather. Forecasters are increasingly flagging the risk of a “Godzilla el Niño” for the 2026-2027 season. Model probabilities for a very strong (Niño-3.4 ≥ +2.0°C) event have risen sharply since the spring; National Oceanic & Atmospheric Administration (NOAA) and Climate Prediction Center (CPC) now puts the probability that El Niño develops and persists through year-end in the 88–94% range, with roughly a one-in-four to one-in-two chance that it crosses into super-Niño territory, peaking around the November–February window.

Taken together, these developments point to heightened inflationary pressure over the next one to two years. Higher energy prices will filter through most, if not all, economic activity. At the same time, the loss of up to 30% of global urea trade, combined with an incoming El Niño season, threatens to depress crop yields and push food prices higher. The reduction in helium supply adds another layer of pressure, weighing on the semiconductor industry and likely lifting prices for chips used across data centres, personal computers and smartphones.

Inflation, in other words, looks set to persist.

Parameta Solutions aggregates broker-contributed data from TP ICAP’s global energy broking desks across energy and commodities markets, providing independent, granular pricing data and liquidity insights to support price discovery, hedging and stronger risk control.

To learn more about our Energy & Commodities data solutions, please contact us for a data sample.

Disclaimer

© 2026 ICAP Information Services Limited (“IISL”). This communication is provided by ICAP Information Services Limited or a member of its group (“Parameta”) and all information contained in or attached hereto (the “Information”) is for information purposes only and is confidential. Access to the Information by anyone other than the intended recipient is unauthorised without Parameta’s prior written approval. The Information may not be not used or disclosed for any purpose without Parameta’s prior written approval, including without limitation, storing, copying, distributing, licensing, selling or displaying the Information, using the Information in an application or to create derived data of any kind, co-mingling the Information with any other data or using the data for any unlawful purpose of for any purpose that would cause it to become a benchmark under any law, regulation or guidance. The Information is not, and should not be construed as, a live price, an offer, bid, recommendation or solicitation in relation to any financial instrument or investment or to participate in any particular trading strategy or constituting financial or investment advice or a financial promotion. The Information does not constitute a public offer under any applicable legislation or an offer to sell or a solicitation of an offer to buy any securities. The Information is not to be relied upon for any purpose whatsoever and is provided “as is” without warranty of any kind, either expressly or by implication, including without limitation as to completeness, timeliness, accuracy, continuity, merchantability or fitness for any particular purpose. All representations and warranties are expressly disclaimed, to the fullest extent possible under applicable law. In no circumstances will Parameta be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of or any inability to use the Information, or any inaccuracy in the Information. Parameta may suspend, withdraw or modify or change the terms of the provision of the Information at any time in its sole discretion, without notice. All rights, including without limitation intellectual property rights, in and to the Information are, and shall remain, the property of IISL or its licensors. Use of, access to or delivery of Parameta’s products and/or services requires a prior written licence from Parameta or its relevant affiliates. The terms of this disclaimer are governed by the laws of England and Wales.

Latest Insights

See All

10 things to know about freight data

Brent just repriced war premium in a week