Interest rate swaps are financial contracts where two parties exchange interest payment streams, typically swapping a fixed rate for a floating rate or vice versa. The core difference between fixed vs floating rate swaps comes down to predictability versus flexibility: fixed rate payments stay constant throughout the contract, while floating rates reset periodically based on market benchmarks. Understanding this distinction is essential for anyone managing interest rate exposure or hedging debt portfolios.

Fixed vs Floating Rate Swaps: Quick Comparison

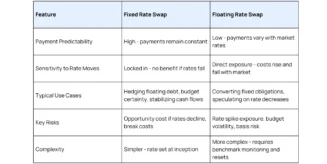

Before diving deeper, let’s look at how these two approaches stack up against each other in practical terms:

What Is an Interest Rate Swap?

An interest rate swap is a derivative contract where two parties agree to exchange interest payment obligations on a specified notional amount. The notional principal itself never changes hands – it’s simply the reference amount used to calculate the interest payments.

Every swap has two “legs”: one party pays based on one interest rate structure while receiving payments based on another. Settlement happens on a net basis, meaning only the difference between the two payment streams actually changes hands. If you owe $100,000 and are due to receive $85,000, you’d simply pay the $15,000 difference.

The beauty of this structure is that it allows organizations to modify their interest rate exposure without restructuring underlying debt or assets. A company with floating-rate debt can effectively convert it to fixed-rate exposure through a fixed rate swap, without actually refinancing the original loan.

How Fixed and Floating Payments Work

The fixed leg of a swap is straightforward. At the outset, both parties agree on a fixed interest rate that will apply for the life of the contract. This swaps rate is typically based on prevailing market conditions at execution and remains unchanged regardless of what happens in the broader economy.

The floating leg works differently. It resets at regular intervals-monthly, quarterly, or semi-annually-based on a reference benchmark rate. The floating rate is typically set at the beginning of each period and paid at the end.

Common floating benchmarks have evolved significantly in recent years. SONIA (Sterling Overnight Index Average) is standard for sterling-denominated swaps, while SOFR (Secured Overnight Financing Rate) has become the dominant benchmark for U.S. dollar swaps following the phase-out of LIBOR. Other regional benchmarks include €STR for the euro and TONA for the Japanese yen.

Pay Fixed vs Receive Fixed

The terminology around swap positions can be confusing at first, but it’s essential to understand which side of the trade you’re on.

Pay Fixed, Receive Floating (Payer Swap)

In a payer swap, you agree to pay a fixed rate while receiving floating rate payments. This is the most common structure for hedging floating-rate debt.

Here’s a concrete scenario: your company has a $10 million loan with interest tied to SOFR plus 200 basis points. You’re concerned rates might spike, so you enter a payer swap where you pay 4.5% fixed and receive SOFR. Now your net position is effectively fixed at 6.5% (4.5% paid on swap + 2% spread on loan – SOFR received on swap + SOFR paid on loan). If SOFR jumps to 6%, you’re still paying that same 6.5% net rate.

Receive Fixed, Pay Floating (Receiver Swap)

A receiver swap flips the structure. You receive fixed payments and pay floating. This position is less common but useful in specific circumstances.

Imagine you’re an insurance company with assets that pay a fixed rate, but you’ve issued liabilities indexed to a floating rate. You could enter a receiver swap to match your cash flows better. Or perhaps you’re speculating that rates will decline – you’d benefit from paying lower floating rates while continuing to receive the higher fixed rate locked in at the swap’s inception.

Simple Example of Fixed vs Floating

Let’s walk through a practical example that shows how the choice between fixed and floating affects your actual costs.

ABC Manufacturing has a $5 million revolving credit facility with interest at SOFR + 1.75%. Their CFO is building next year’s budget and needs to decide whether to enter a fixed rate swap or stay floating.

Option 1: Stay Floating

They pay whatever SOFR is each quarter plus their 1.75% spread. If SOFR starts at 4.5% but rises to 5.5% by year-end, their costs increase from $312,500 per quarter to $362,500 – a budget variance that creates planning headaches.

Option 2: Enter a Fixed Rate Swap

They execute a payer swap at 4.25% fixed. Now their effective rate is locked at 6% (4.25% + 1.75%), producing quarterly interest costs of $300,000 regardless of where SOFR moves. The CFO can budget with certainty.

But here’s the trade-off: if SOFR actually falls to 3.5% by year-end, the floating option would have been cheaper. The company pays for certainty by giving up the potential benefit of falling rates. That’s the fundamental tension in fixed vs floating rate swaps.

Key Risks and Practical Considerations

Fixed Rate Swaps

- Opportunity cost: If market rates decline significantly after you’ve locked in a fixed rate, you miss out on potential savings

- Break costs: Unwinding a fixed rate swap before maturity can be expensive, especially if rates have moved against your position

- Duration mismatch: If your underlying debt matures or gets refinanced before the swap term ends, you’re left with a naked hedge position

- Credit exposure: You’re exposed to the counterparty’s ability to make payments throughout the swap’s life

Floating Rate Swaps

- Budget volatility: Your interest costs fluctuate with market conditions, making financial planning more difficult

- Rate spike risk: A sudden jump in benchmark rates can dramatically increase your costs

- Basis risk: The floating benchmark in your swap might not move perfectly in sync with the rate on your underlying debt

- Reset complexity: You need systems and processes to track benchmark fixings and calculate payments for each period

Common Risks for All Swaps

- Counterparty risk: The risk that your swap counterparty defaults on their obligations

- Collateral requirements: Most swaps now require posting collateral based on mark-to-market values, which can strain liquidity

- Documentation complexity: Swaps are governed by detailed legal agreements (typically ISDA Master Agreements) that require careful negotiation

- Accounting treatment: Hedge accounting under standards like IFRS 9 or ASC 815 can be complex and requires ongoing documentation

Strategic Considerations

- Interest rate outlook: Your view on future rate movements should inform whether you want fixed or floating exposure

- Business model alignment: Companies with predictable cash flows often prefer fixed rates, while those with more variable revenues might opt for floating

- Portfolio approach: Many sophisticated treasurers maintain a mix of fixed and floating exposure rather than going all-in on one structure

- Tenor matching: Align your swap maturity with the underlying exposure you’re hedging to avoid basis risk

Learn more about hedging interest rate risks in our piece exploring the topic in further detail.

Markets We Cover

When tracking swap rates and market movements, market participants need reliable, comprehensive data across multiple tenors, currencies, and rate structures. This is where Parameta Solutions makes a tangible difference.

Our Indicative Data service delivers real-time and historical swap rate data across major currency pairs and tenors. Whether you’re marking positions to market or analyzing rate trends, you get access to continuously updated curves that reflect current market conditions. The data covers vanilla fixed-for-floating swaps, basis swaps, and overnight index swaps (OIS), with granular tenor breakdowns from overnight to 50 years.

For documentation and valuation disputes, Evidential Data provides time-stamped, auditable records of market rates at specific points in time. This becomes critical when you need to demonstrate what rate was prevailing at a particular moment – whether for accounting close, litigation support, or regulatory reporting.

The Benchmarks & Indices offering includes proprietary reference rates calculated using robust methodologies. These can serve as contractual reference rates in swap agreements or as independent verification against other benchmark sources.

What sets Parameta Solutions apart is the methodology rigor. Our rates are derived from actual executable prices and transactions, not just indicative quotes, giving you confidence in their reliability for critical decisions like hedge effectiveness testing or collateral valuations.

Need More Information on Swap Rates and Market Data?

Speak with our team to learn how Parameta Solutions can support your interest rate risk management strategy.

About Parameta OTC Market Data

Parameta is the exclusive provider of OTC market data from TP ICAP’s leading brokerage brands, including ICAP, Tullett Prebon, and PVM.

We deliver high quality market data, indices, and analytics across interest rate swaps and options, money markets, inflation, FX, energy and commodities.

Our solutions empower buyside companies with trusted insights to support trading strategy development, price discovery, pre and post trade analytics, risk management, and regulatory compliance.

Contact us for more information or to request a data sample.

Frequently Asked Questions

What is the difference between a fixed and floating interest rate swap?

The primary difference lies in payment certainty. In a fixed rate swap, one party pays a predetermined interest rate that doesn’t change over the life of the contract, providing complete predictability. A floating rate swap involves payments that reset periodically based on a benchmark rate like SOFR or SONIA, meaning payment amounts vary with market conditions. Fixed swaps trade flexibility for certainty, while floating swaps maintain market exposure but offer no protection against rate increases.

What does pay fixed receive floating mean in an interest rate swap?

Pay fixed receive floating (also called a payer swap) means you agree to pay a fixed interest rate while receiving floating rate payments based on a benchmark. This structure is typically used to hedge floating-rate debt. For example, if you have a loan at SOFR + 2% and enter a payer swap where you pay 4% fixed and receive SOFR, your net cost becomes fixed at 6% regardless of where SOFR moves. You’ve effectively converted floating-rate debt into a fixed-rate obligation.

What does receive fixed pay floating mean in an interest rate swap?

Receive fixed pay floating (also called a receiver swap) means you receive a predetermined fixed rate while paying a floating rate that resets periodically. This position is less common but useful when you have fixed-rate assets and floating-rate liabilities, or when you believe interest rates will decline. If you’re receiving 5% fixed but paying SOFR that drops from 4% to 3%, you benefit from the spread between the fixed rate you receive and the lower floating rate you pay.

Disclaimer

© 2026 ICAP Information Services Limited (“IISL”). This communication is provided by ICAP Information Services Limited or a member of its group (“Parameta”) and all information contained in or attached hereto (the “Information”) is for information purposes only and is confidential. Access to the Information by anyone other than the intended recipient is unauthorised without Parameta’s prior written approval. The Information may not be not used or disclosed for any purpose without Parameta’s prior written approval, including without limitation, storing, copying, distributing, licensing, selling or displaying the Information, using the Information in an application or to create derived data of any kind, co-mingling the Information with any other data or using the data for any unlawful purpose of for any purpose that would cause it to become a benchmark under any law, regulation or guidance. The Information is not, and should not be construed as, a live price, an offer, bid, recommendation or solicitation in relation to any financial instrument or investment or to participate in any particular trading strategy or constituting financial or investment advice or a financial promotion. The Information does not constitute a public offer under any applicable legislation or an offer to sell or a solicitation of an offer to buy any securities. The Information is not to be relied upon for any purpose whatsoever and is provided “as is” without warranty of any kind, either expressly or by implication, including without limitation as to completeness, timeliness, accuracy, continuity, merchantability or fitness for any particular purpose. All representations and warranties are expressly disclaimed, to the fullest extent possible under applicable law. In no circumstances will Parameta be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the Information. Parameta may suspend, withdraw or modify or change the terms of the provision of the Information at any time in its sole discretion, without notice. All rights, including without limitation intellectual property rights, in and to the Information are, and shall remain, the property of IISL or its licensors. Use of, access to or delivery of Parameta’s products and/or services requires a prior written licence from Parameta or its relevant affiliates. The terms of this disclaimer are governed by the laws of England and Wales.