Recent developments in Middle Eastern transit flows are not only driving oil prices higher, but they are also reshaping the structure of the crude forward curve in ways that materially impact hedging effectiveness and valuation frameworks.

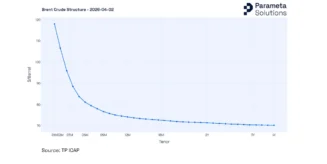

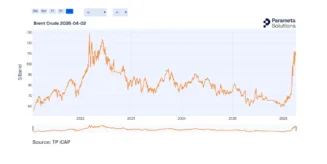

As of early April 2026, Brent front month contracts are trading near $119/bbl.*, while deferred maturities have remained anchored closer to the $70–75* range beyond the two-year point.

This ~$50* front-to-back spread represents one of the steepest episodes of backwardation in the modern Brent dataset, exceeding even the June 2022 dislocation following the Russia–Ukraine invasion.

While listed benchmarks have reacted immediately to the disruption of approximately 10–15 million barrels per day of Hormuz linked transit flows since March 4, curve deformation of this magnitude introduces a different category of market risk, one did not capture by flat price exposure alone.

*Source: TP ICAP

When Supply Risk Becomes a Curve Risk

Extreme backwardation is typically associated with immediate supply tightness.

In this instance, the Brent BOM–M12 time spread has widened rapidly from ~$10 to ~$35* in the four weeks following the Strait closure, a rate of acceleration which exceeds that observed during the 2022 geopolitical shock.

From a trading perspective, this suggests that the market is pricing acute short-term logistical stress while simultaneously anticipating resolution within the 6–12-month horizon, reflected by deferred contracts converging closer to long-term equilibrium near $70–71/bbl*.

However, curve implied normalization does not necessarily translate into stable executable pricing across delivered cargoes, regional differentials or freight adjusted arbitrage levels, particularly where transit constraints alter routing economics rather than outright production.

*Source: TP ICAP

In such environments:

- front month futures may track benchmark expectations

- but delivered physical cargos may clear at materially different premiums

- location specific blends may reprice independently

- forward differentials may widen unevenly across basins

Introducing potential divergence between hedge instruments and underlying crude exposures.

Hedge Instrument vs Exposure: A Basis Alignment Challenge

Many physical market participants hedge prompt exposure using exchange listed benchmarks such as ICE Brent futures.

During logistics‑driven disruptions, Brent‑linked seaborne crude, which underpins the global benchmark complex, may also absorb an additional transportation risk premium not always reflected in listed settlement prices.

While ICE Brent futures are designed to capture expectations of global supply risk, physically delivered cargoes are priced based on the executable cost of transporting crude through constrained shipping lanes. When transit routes are disrupted, refiners requiring prompt delivery may face increased freight rates, insurance premia, voyage uncertainty or rerouting costs, all of which can be incorporated into delivered cargo differentials before they are reflected in benchmark futures levels.

As a result, seaborne Brent‑linked grades may clear at materially higher forward premiums relative to exchange‑listed indications, introducing potential divergence between hedge benchmarks and the executable price of physically deliverable supply.

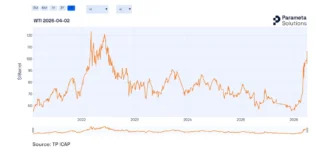

Concurrently, landlocked U.S. supply continues to buffer WTI linked domestic markets, contributing to widening interbenchmark basis as approximately 10 million barrels per day* of Hormuz dependent exports remain disrupted.

The first week of April 2026, prior to the announcement of a temporary transit truce, nearby WTI contracts traded at a premium to Brent, an inversion of the relationship typically observed during Middle Eastern supply disruptions.

This reflected the immediate logistical impact of constrained seaborne availability, as refiners requiring prompt physical delivery were forced to source inland U.S. barrels where available, bidding domestic supply higher relative to waterborne Brent‑linked crude.

While the futures inversion was temporary, it underscored the extent to which transit‑driven constraints can alter regional clearing dynamics independently of global benchmark expectations, particularly where prompt delivered supply becomes geographically concentrated.

The resulting misalignment can manifest through:

- slippage between MTM valuation and executable cargo levels

- reduced hedge proxy effectiveness

- distortion in curve derived storage economics

- widening differential risk across refining margins

All of which become particularly relevant when benchmark linked contracts are used to hedge geographically specific physical flows.

Visibility Into Executable Forward Pricing

During periods of structural curve dislocation, managing prompt volatility may depend less on directional outright exposure and more on understanding:

- delivered forward spreads

- regional crude differentials

- freight adjusted arbitrage breakeven

- OTC Brent linked forward pricing

- time spread liquidity beyond the listed curve

Parameta Solutions aggregates broker contributed data from TP ICAP’s global energy broking desks across physical and paper OTC oil markets, providing market participants with real-time visibility into executable forward pricing that may not be fully reflected in exchange-based benchmarks.

- Unmatched barrel coverage: Crude, light ends, middle distillates, fuel oil and LPG, backed by data from three of the world’s largest oil brokers.

- Execution‑grade, real‑time pricing: Broker‑sourced mid‑prices designed to support fast, accurate decision‑making.

Where geopolitical risk transmits through logistics constraints rather than production loss, insight into where the physical clears, not solely where the future settles, can play a key role in hedging, valuation, and risk management workflows.

To access more information about our Energy & Commodities data solutions, please contact us for a data sample or further information.

Disclaimer

© 2026 ICAP Information Services Limited (“IISL”). This communication is provided by ICAP Information Services Limited or a member of its group (“Parameta”) and all information contained in or attached hereto (the “Information”) is for information purposes only and is confidential. Access to the Information by anyone other than the intended recipient is unauthorised without Parameta’s prior written approval. The Information may not be not used or disclosed for any purpose without Parameta’s prior written approval, including without limitation, storing, copying, distributing, licensing, selling or displaying the Information, using the Information in an application or to create derived data of any kind, co-mingling the Information with any other data or using the data for any unlawful purpose of for any purpose that would cause it to become a benchmark under any law, regulation or guidance. The Information is not, and should not be construed as, a live price, an offer, bid, recommendation or solicitation in relation to any financial instrument or investment or to participate in any particular trading strategy or constituting financial or investment advice or a financial promotion. The Information does not constitute a public offer under any applicable legislation or an offer to sell or a solicitation of an offer to buy any securities. The Information is not to be relied upon for any purpose whatsoever and is provided “as is” without warranty of any kind, either expressly or by implication, including without limitation as to completeness, timeliness, accuracy, continuity, merchantability or fitness for any particular purpose. All representations and warranties are expressly disclaimed, to the fullest extent possible under applicable law. In no circumstances will Parameta be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the Information. Parameta may suspend, withdraw or modify or change the terms of the provision of the Information at any time in its sole discretion, without notice. All rights, including without limitation intellectual property rights, in and to the Information are, and shall remain, the property of IISL or its licensors. Use of, access to or delivery of Parameta’s products and/or services requires a prior written licence from Parameta or its relevant affiliates. The terms of this disclaimer are governed by the laws of England and Wales.