Versatile OTC interest rate derivatives market data for essential investment applications

The Secured Overnight Financing Rate (SOFR) is a broad measure of the cost of borrowing cash overnight collateralized by Treasury securities. The SOFR includes all trades in the Broad General Collateral Rate plus bilateral Treasury repurchase agreement (Repo) transactions cleared through the Delivery-versus-Payment (DVP) service offered by the Fixed Income Clearing Corporation (FICC), which is filtered to remove a portion of transactions considered “specials”.

Note that specials are Repos for specific-issue collateral, which take place at cash-lending rates below those for general collateral Repos because cash providers are willing to accept a lesser return on their cash in order to obtain a particular security.

How is SOFR calculated?

The SOFR is calculated as a volume-weighted median of transaction-level tri-party Repo data collected from the Bank of New York Mellon as well as GCF Repo transaction data and data on bilateral Treasury Repo transactions cleared through FICC’s DVP service, which are obtained from the US Department of the Treasury’s Office of Financial Research (OFR). Each business day, the New York Fed publishes the SOFR on the New York Fed website at approximately 8:00 a.m. ET.

For more information on the SOFR’s publication schedule and methodology, see Additional Information about Reference Rates Administered by the New York Fed.

SOFR is based on actual transactions in the US Treasury Repo market, making it more transparent and reliable compared to previous benchmarks like LIBOR. Grounded in observable data, SOFR reduces the risk of rate manipulation. With regulators mandating the transition from LIBOR to SOFR, using SOFR products ensures compliance with new regulatory standards. It has been widely adopted in financial markets, providing liquidity and broad acceptance that benefit trading and risk management. SOFR products, such as swaps and options, offer effective tools for managing interest rate risk, especially in a volatile market environment. The variety of SOFR-linked products—including cross-currency swaps, basis swaps, and interest rate options—allows clients to tailor strategies to specific needs and market conditions.

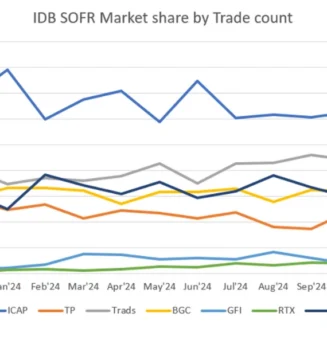

SOFR Data: The Parameta Advantage

Parameta Solutions is the exclusive provider of unique market data sourced from TP ICAP, the world’s largest interdealer broker. With 2,600 brokers operating in 28 countries, TP ICAP provides access to deep liquidity pools.

SOFR Products Overview

Parameta offers data sourced from both ICAP and TP, which offer a comprehensive suite of products linked to the Secured Overnight Financing Rate (SOFR), catering to various market needs. These products are designed to support trading, risk management, and analytics in the evolving interest rate landscape.

SOFR Short and Medium Term Curve

- Short Term Curve: Provides insights into the near-term expectations of interest rates.

- Medium Term Curve: Offers a broader view of interest rate trends over a longer horizon.

Risk-Free Cross Currency (CCY) Swaps and Basis Swaps

- Cross Currency Swaps: Facilitate the exchange of principal and interest payments in different currencies ranging from G10 to Emerging Currency, benchmarked against USD SOFR.

- Basis Swaps: Allow for the exchange of floating interest rate payments between SOFR and other benchmarks like ESTR and SONIA.

Meeting Dates and Single Period Swaps

Key FOMC dates for central bank meetings and policy announcements that impact SOFR rates. We also have Short Term IMM Dates.

Invoice Spread and Convexity Grid

TP also has a short term SOFR Convexity Grid, ICAP is developing SwapPX Invoice Spread page as a joint product with CME and their Cheapest to Deliver and Future pricing.

Basis Swaps Between Various Benchmarks

Basis swaps between SOFR and other USD benchmarks provide flexibility in managing interest rate exposure across different financial instruments. Both Brands have Fed Fund vs SOFR Basis Swaps. TP has SOFR vs Prime and SOFR vs T-Bills as well.

Interest Rate Options (ATM, Skew OTM, and Cap Floors)

Our SOFR Swaption SOFR Discounting interest rate options and Cap Floor are available for both ICAP AND TP. We are currently working to expand SOFR CMS Spread Over offering for both brands.

Available Data Packages

TP Products

- Medium and Short Term Curves and Swaps: Available in the TP SOFR Package, TP Risk Free Package, and SwapMarker.

- Risk Free SOFR USD Swaps: Available in the TP SOFR Package, TP Risk Free Package, and SwapMarker.

- Risk-Free Cross CCY Swaps and Basis Swaps: Included in the TP Risk Free Package.

- TP SOFR IRO: Part of the TP IRO Package.

ICAP Products

- Medium and Short Term Curves and Swaps: Found in the ICAP Risk Free Package, SwapPX, and RCM 19901.

- Risk Free SOFR USD Swaps: Available in the ICAP Risk Free Package, SwapPX and RCM 19901

- Risk-Free Cross CCY Swaps and Basis Swaps: Available in the Interest Rate Derivative Package

- ICAP IRO: Available in the Derivative Package and the IRO Direct Package.

These products leverage the liquidity and expertise of ICAP and TP, ensuring robust support for market participants navigating the transition to SOFR.

Related Solutions

Trust Parameta for comprehensive SOFR-related datasets, sourced from TP ICAP.

Related Solutions

Trust Parameta for comprehensive SOFR-related datasets, sourced from TP ICAP.

Capital Markets Indicative Data

High-quality, independent market data to improve trading strategies, enhance risk management, and meet regulatory requirements — offering a trusted, conflict-free view of the markets.

Disclaimer

© 2026 ICAP Information Services Limited (“IISL”). This communication is provided by ICAP Information Services Limited or a member of its group (“Parameta”) and all information contained in or attached hereto (the “Information”) is for information purposes only and is confidential. Access to the Information by anyone other than the intended recipient is unauthorised without Parameta’s prior written approval. The Information may not be not used or disclosed for any purpose without Parameta’s prior written approval, including without limitation, storing, copying, distributing, licensing, selling or displaying the Information, using the Information in an application or to create derived data of any kind, co-mingling the Information with any other data or using the data for any unlawful purpose of for any purpose that would cause it to become a benchmark under any law, regulation or guidance. The Information is not, and should not be construed as, a live price, an offer, bid, recommendation or solicitation in relation to any financial instrument or investment or to participate in any particular trading strategy or constituting financial or investment advice or a financial promotion. The Information does not constitute a public offer under any applicable legislation or an offer to sell or a solicitation of an offer to buy any securities. The Information is not to be relied upon for any purpose whatsoever and is provided “as is” without warranty of any kind, either expressly or by implication, including without limitation as to completeness, timeliness, accuracy, continuity, merchantability or fitness for any particular purpose. All representations and warranties are expressly disclaimed, to the fullest extent possible under applicable law. In no circumstances will Parameta be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of, any inability to use, or any inaccuracy in the Information. Parameta may suspend, withdraw or modify or change the terms of the provision of the Information at any time in its sole discretion, without notice. All rights, including without limitation intellectual property rights, in and to the Information are, and shall remain, the property of IISL or its licensors. Use of, access to or delivery of Parameta’s products and/or services requires a prior written licence from Parameta or its relevant affiliates. The terms of this disclaimer are governed by the laws of England and Wales.