Key Takeaways:

- Overnight Index Swaps (OIS) are derivative contracts that exchange a fixed interest rate for a floating rate based on overnight indices like the USD Secure Overnight Financing Rate ( SOFR) or the GBP Sterling Overnight Index Average, SONIA ), typically used by financial institutions for risk management and speculation.

- OIS rates serve as crucial benchmarks for risk-free rates in financial markets, with the SONIA currently trading at 3.73% as of February 17, 2026, while historical data shows significant fluctuations in response to monetary policy changes.

- Calculating an OIS payment involves geometric compounding of the daily overnight rates observed during the contract period.

What is an Overnight Index Swap?

An overnight index swap (OIS) is a derivative contract between two parties to exchange interest payments over a specified period. One party pays a fixed rate, while the other pays a floating rate based on a daily overnight index rate.

They typically involve commercial banks, investment banks, hedge funds, or corporations and central banks, who set the underlying rates.

How Do Overnight Index Swaps Work

OISs function where one party pays a fixed interest rate, whilst the other pays a floating rate based on an overnight index (such as SONIA in the UK, SOFR in the U.S. or €STR in European zone, just to name a few).

At maturity, only the net difference between the two payment streams is exchanged, rather than the full notional amounts, meaning that the one with the higher amount pays the net difference to the other party.

As an example, if the floating rate is higher than the fixed rate, the party for the floating rate pays the difference between the floating rate and fixed rate to the other party.

The OIS is used by financial institutions to hedge interest rate risks. We mention risk because interest rates fluctuate over time, and OIS can help manage this.

How the Mechanisms of an OIS work

OIS contracts operate through a straightforward mechanism. The floating rate payer tracks the daily overnight rate throughout the contract period, and these rates are geometrically compounded to produce a single effective rate at maturity. This compounding reflects how overnight positions would actually accumulate if rolled forward each day. The fixed rate payer, meanwhile, simply applies their predetermined rate to the notional amount. Only the net difference between these two calculated amounts changes hands at settlement.

What is a Forward OIS?

Works in a similar way to the OIS, where a fixed rate leg is exchanged for a floating rate leg. One party will pay the fixed rate amount, and the other party pays the floating rate amount based on the daily overnight index rate.

The difference: For a forward OIS transaction, the fixed rate is locked now (today) and will start at a future date. The most popular type of forward OIS are the ones that track Central Bank meeting dates because the largest OIS repricing occurs around policy meetings.

Benefits:

- Hedging against risks such as future interest rate volatility due to central bank policy expectations.

- Manage risks

- Reduce counter-party risks – In situations where another party defaults.

Forward OIS is a great way to manage short-term interest fluctuations and risks.

Who are Overnight Index Swaps for?

OISs are primarily designed for:

- Financial institutions seeking to hedge against short-term interest rate risk

- Banks managing their funding costs and interest rate exposures

- Central banks and monetary policy makers who use OIS rates as indicators of market expectations

- Institutional investors looking to manage portfolio interest rate sensitivity

- Corporations with significant exposure to short-term interest rate fluctuations

How to Use Overnight Index Swaps

When it comes to the usage of OISs, they are typically used for the purposes of risk management via various means. These can include:

- Hedging against interest rate risks: Financial institutions, banks and investors would make use of an OIS as it protects them from short-term interest rate risks, as interest rates fluctuate.

- Speculation: Traders make use of an OIS for possible profit gains. With traders speculating when interest rates will go up/down, they can enter an OIS with a bank, in which traders receive a floating rate and pay a fixed rate, while the banks pay the floating rate and receive the fixed rate.

- Managing funded costs: Entering into an OIS contract allows money to be locked, in which helps banks, financial institutions all protect and manage funds.

How is the Overnight Index Swap (OIS) Rate Calculated?

Calculating the OIS rate involves finding the overnight index, whether that be the SOFR (U.S.), SONIA (UK), €STR (European), among others. Thereafter, it is calculating the compounded interest rate for a set period (referred to as the maturity rate) of the floating leg and then finding the fixed rate that will be deducted by the floating rate to find the net settlement.

The fixed rate is agreed upon at the start of the contract, and both the fixed and floating rates are presented as percentages.

The calculation breakdown:

- Notional: Fixed amount (total)

- Maturity: Period

- Fixed rate: percentage on the notional

- Floating rate: compounded daily on the overnight index chosen. For example, SOFR (U.S.) or SONIA (UK).

Every day the overnight rate is observed. Floating leg compounds each day’s rate for the maturity. At maturity if the compounded rate or floating rate is higher than the fixed rate than the difference is owed by the floating rate payer.

Here’s a practical example:

Bank A enters a one-year OIS with Bank B on a notional amount of $100 million.

Bank A agrees to pay a fixed rate of 3.75%, while Bank B pays the average of the daily SOFR over that year. At maturity, only the net difference is exchanged.

If the average SOFR turns out to be 3.90%, Bank A receives the difference of 0.15% on $100 million, which equals $150,000.

This settlement mechanism makes OIS particularly capital-efficient compared to other interest rate products.

What Are the Benefits of an Overnight Index Swaps?

OIS rates serve as the foundation for discounting in derivatives valuation, meaning accurate OIS swap data directly improves the accuracy of balance sheet valuations. Some of the key benefits that can be found through effective utilisation of OISs are:

- Risk Management Benefits: OIS contracts provide precise tools for managing interest rate exposure without introducing credit risk complications. Unlike traditional interest rate swaps referenced to interbank offered rates, OIS isolates pure policy rate risk. This makes hedging more effective and reduces basis risk. Banks use OIS to hedge their deposit bases, which typically reprice in line with central bank policy rates rather than term lending rates. The capital efficiency of net settlement also means institutions can maintain larger hedge positions without tying up excessive collateral.

- Pricing and Transparency Benefits: The robust liquidity in OIS markets creates transparent pricing and tight bid-ask spreads, particularly in major currencies. This liquidity translates to lower transaction costs and more reliable valuation for complex portfolios.

- Hedging: As mentioned above, financial institutions, banks and investors would make use of an OIS as it protects them from short-term interest rate risks, as interest rates fluctuate.

- Low counterparty risk: There is still a possible default in which money could be at risk. The default could happen if one party does not fulfill payment or does not uphold their part in the contract, as one example. OIS is a good option, but it does not mean that there is zero risks with it.

Risks associated with Overnight Index Swaps

Overnight index swaps are a good option for traders, investors, financial institutions and central banks as they can help prevent a lot of risks and is a way to manage funds. With that being said, it does not mean that there are no risks that come with them, and it is important to be aware of them before deciding on an OIS. These risks can include:

- Counter party risks: If a default happens. The default could happen if one party does not fulfill payment or does not uphold their part in the contract, as one example

- Interest rate fluctuations: The primary risk in OIS transactions is interest rate risk and the possibility that rate movements will favor your counterparty.

- Credit risk: This exists but remains relatively low compared to other derivatives since OIS contracts typically involve net settlement and often include collateral arrangements.

Contact Parameta Solutions

Overnight index swaps represent a fundamental tool in modern interest rate risk management, offering financial institutions a capital-efficient way to hedge short-term rate exposures while maintaining pricing transparency. From hedging deposit bases to speculating on policy rate movements, OIS contracts provide flexibility that traditional interest rate products often can’t match.

At Parameta Solutions, we understand the data challenges that come with managing interest rate derivatives portfolios. We provide OIS data to enhance transparency in your decisions. If you would like to view our OIS SOFR data sample, you can download here. Our capital markets solutions provide the data and analytics infrastructure you need to value, manage, and report on OIS positions with confidence.

If you’re looking to strengthen your interest rate risk management capabilities or need better data infrastructure for your derivatives operations, we’d be glad to discuss how our solutions can support your specific needs. Reach out to our team to learn more.

Frequently Asked Questions

Is OIS a Risk-Free Rate?

OIS (Overnight Index Swap) is considered near risk-free rather than completely risk-free. It reflects the overnight unsecured lending rate between banks and is widely used as a proxy for risk-free rates in financial markets, as it carries minimal credit risk compared to other benchmark rates.

What are the risks of swap exchanges?

- Counterparty risk: the possibility that the other party may default on their obligations

- Market risk: adverse movements in interest rates, exchange rates, or other underlying variables

- Liquidity risk: difficulty in exiting or unwinding the swap position

- Operational risk: errors in documentation, settlement, or processing

Can OIS be turned off?

No, OIS cannot be “turned off” as it is a financial derivative contract with specific terms and maturity dates. However, positions can be unwound or closed out before maturity through an offsetting transaction with a counterparty, though this may involve costs or gains depending on market conditions.

What’s the Difference Between OIS and IRS?

An Interest Rate Swap (IRS) traditionally exchanges a fixed rate for a floating rate based on a term reference rate like LIBOR or EURIBOR. These term rates historically contained both monetary policy expectations and bank credit risk premiums. An OIS, by contrast, references only overnight rates that closely track central bank policy rates, stripping out credit components. This fundamental difference means OIS rates trade below term IRS rates by a spread that reflects bank credit risk and term premiums.

The transition away from LIBOR has blurred these distinctions somewhat. Modern IRS contracts increasingly reference risk-free rates (RFRs) like SOFR or SONIA, which are actually overnight rates similar to OIS. However, these “new” IRS typically use term versions of RFRs or apply conventions like lookback periods that differ from traditional OIS structures. For treasury teams managing interest rate exposure, understanding whether your swap references a term rate or an overnight rate affects everything from hedge effectiveness to accounting treatment. The complexity of managing these different instrument types makes comprehensive market data essential, something that Parameta Solutions addresses through its specialized derivatives data solutions.

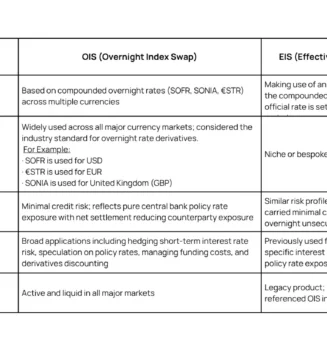

What’s the Difference Between Effective Index Swap (EIS) and the Overnight Index Swap (OIS)?

Overnight Index Swap (OIS) is an interest rate where a fixed rate is exchanged for a floating rate based compounded overnight index like SOFR, SONIA or €STR. One party pays the fixed rate, and another party pays the floating rate linked to the overnight benchmark.

Effective Index Swap (EIS) swaps the fixed rate against the ‘effective rate’ (average of the benchmark rate).

A table has been provided, help clarify the practical differences between OIS and EIS:

How to Calculate OIS?

Calculating an OIS payment involves geometric compounding of the daily overnight rates observed during the contract period.

Floating Payment = Notional × [(∏(1 + ri × di/360) – 1)]

- Where ri represents each daily overnight rate

- di is the number of days that rate applies

- product symbol indicates multiplying across all days in the period.

Fixed Payment = Notional × Fixed Rate × Days/360.

Disclaimer

© 2026 ICAP Information Services Limited (“IISL”). This communication is provided by ICAP Information Services Limited or a member of its group (“Parameta”) and all information contained in or attached hereto (the “Information”) is for information purposes only and is confidential. Access to the Information by anyone other than the intended recipient is unauthorised without Parameta’s prior written approval. The Information may not be not used or disclosed for any purpose without Parameta’s prior written approval, including without limitation, storing, copying, distributing, licensing, selling or displaying the Information, using the Information in an application or to create derived data of any kind, co-mingling the Information with any other data or using the data for any unlawful purpose of for any purpose that would cause it to become a benchmark under any law, regulation or guidance. The Information is not, and should not be construed as, a live price, an offer, bid, recommendation or solicitation in relation to any financial instrument or investment or to participate in any particular trading strategy or constituting financial or investment advice or a financial promotion. The Information does not constitute a public offer under any applicable legislation or an offer to sell or a solicitation of an offer to buy any securities. The Information is not to be relied upon for any purpose whatsoever and is provided “as is” without warranty of any kind, either expressly or by implication, including without limitation as to completeness, timeliness, accuracy, continuity, merchantability or fitness for any particular purpose. All representations and warranties are expressly disclaimed, to the fullest extent possible under applicable law. In no circumstances will Parameta be liable for any indirect or direct loss, or consequential loss or damages including without limitation, loss of business or profits arising from the use of or any inability to use the Information, or any inaccuracy in the Information. Parameta may suspend, withdraw or modify or change the terms of the provision of the Information at any time in its sole discretion, without notice. All rights, including without limitation intellectual property rights, in and to the Information are, and shall remain, the property of IISL or its licensors. Use of, access to or delivery of Parameta’s products and/or services requires a prior written licence from Parameta or its relevant affiliates. The terms of this disclaimer are governed by the laws of England and Wales.

Latest Insights

See All

What is OTC data

What are Credit Default Swaps and How Do They Work?