Equity markets don’t absorb macro change all at once. This paper explores whether interest rate swaps and swaptions data can help interpret how those shifts may be reflected in equity behaviour.

The equity signal you’re not watching

What interest rate swaps and swaptions could reveal about future returns

What the analysis explores

Applying rates data can add equity insight

An exploration of how interest rate swaps and swaptions data could be used outside traditional macro analysis to inform equity thinking.

Early signs of macro change

Shifts in rate levels and rate volatility may help indicate changing equity behaviour before repricing is fully reflected.

Understanding sector sensitivity

Different rate signals can translate into different sector responses as market assumptions evolve.

An additional equity lens

Explores how this approach could sit alongside traditional equity research and portfolio analysis.

What the analysis showed

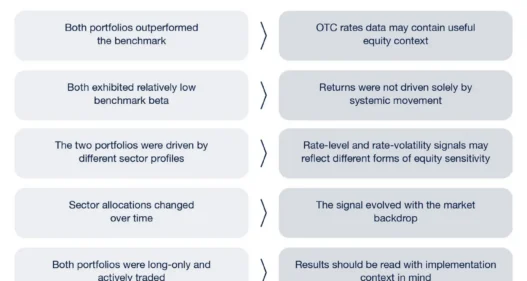

Two model-based, long-only equity portfolios were constructed using swaps and swaptions data. Across the analysis period, both exhibited distinct patterns, suggesting how different rate signals may be reflected in equity behaviour.

Download the full report

Access insights into how swaps and swaptions data can help interpret equity behaviour, sector sensitivity and early signals of macro change.